Weekly Market Commentary - April 5th, 2025 - Click Here for Past Commentaries

-

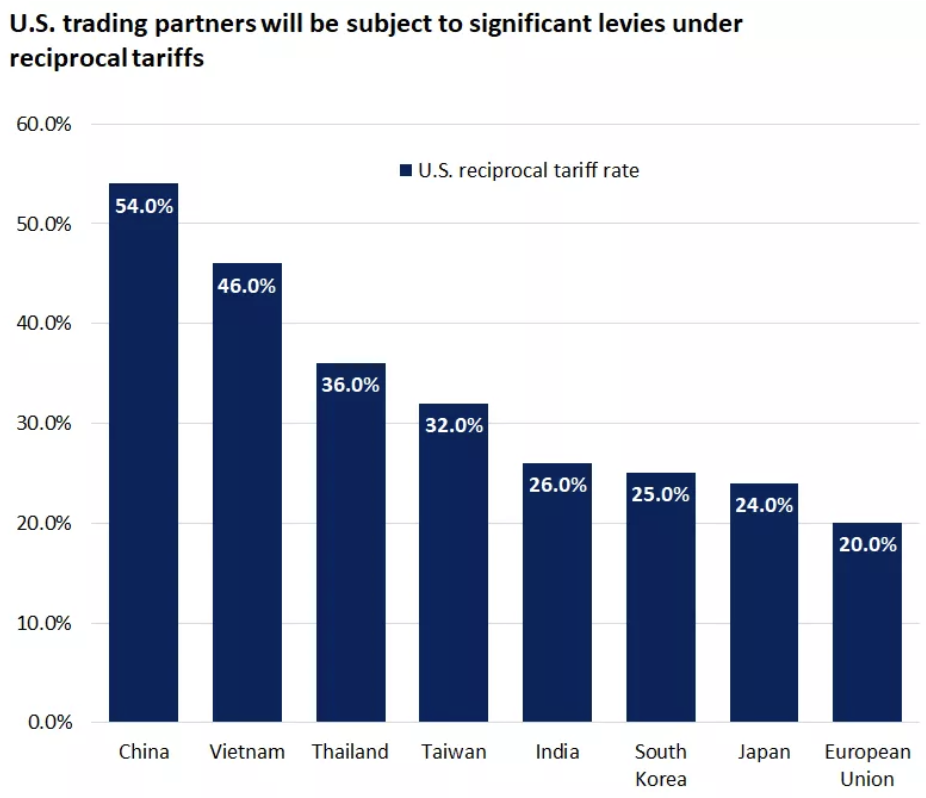

On April 2, President Donald Trump announced U.S. reciprocal tariff plans that were more

aggressive than expected. A 10% minimum tariff will apply to all imports coming into the U.S.

beginning April 5 while higher tariffs will be charged on countries that the U.S. has larger

trade deficits with. The new tariffs are estimated to raise the effective tariff rate on U.S.

imports from 2.3% in 2024 to between 20% - 25%, the highest in at least 100 years.

China announced retaliatory tariffs, matching the U.S. reciprocal tariff rate of 34%.

The tariff announcement, and China's retaliation, drove risk-off sentiment in markets, with

equities finishing the week sharply lower and U.S. Treasury yields declining to their lowest

since October 2024.

Tariffs pose a headwind to U.S. economic growth and put upward pressure on prices in the near

term. However, the U.S. economy is entering this period from a position of strength. Additionally,

the Federal Reserve is likely to step in to support softening economic growth if labor-market

conditions show meaningful signs of weakening.

While volatility is never comfortable, we recommend investors stick with their long-term investment

strategy, with an emphasis on quality and diversification. Avoid making emotionally charged investment

decisions, and remember that time in the market has proven to be a better strategy over time than trying

to time yourself in and out of the market.

-

The magnitude of the announced tariffs will likely serve as a headwind to U.S. economic growth.

Tariffs can pressure corporate profit margins through higher input costs and weigh on household

spending through lower inflation-adjusted incomes. Consumer-spending data has already shown signs

of slowing in the first months of 2025, as the uncertain policy backdrop has weighed on sentiment.

Additionally, retaliatory measures, such as those taken by China, can weigh on activity in

businesses that are reliant on exports to drive sales.

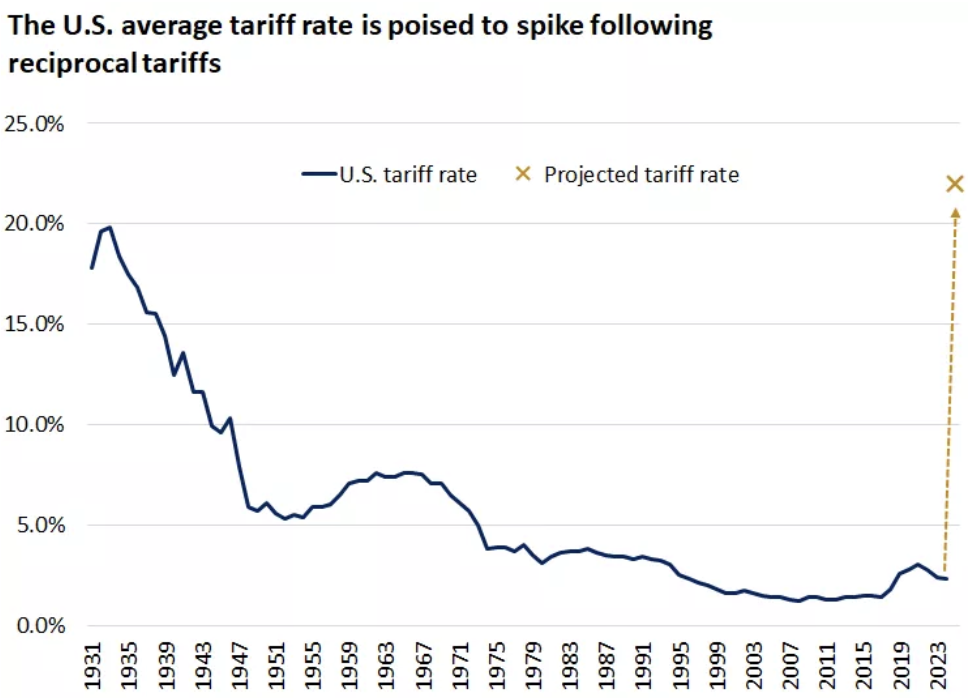

From 2000 - 2024, the average U.S. tariff rate for all imports was a modest 1.7%. Based on the announced tariffs, the average U.S. tariff rate is expected to jump to between 20% – 25%.2 In 2024, the U.S. economy imported roughly $3.3 trillion of goods.3 Assuming an average tariff rate of 20%, this would equate to tariff revenue of roughly $660 billion, or roughly 2.3% of 2024 GDP.

-

How the incremental revenue from tariffs is used will be critical in determining the economic

impact. If a large portion of this revenue is deployed to areas that promote growth, such as

financing lower taxes, economic growth could hold up better. However, if a majority of the

additional tariff revenue is used to reduce the U.S. fiscal deficit, U.S. economic growth

could slow more meaningfully.

While tariffs will serve as a headwind to economic growth, the U.S. economy is entering this period from a position of strength.

* Real GDP has expanded at an above-trend pace over the past two years, and S&P 500 earnings per share grew by 18% in the fourth quarter, the strongest growth rate since the fourth quarter of 2021.3 * Household balance sheets remain healthy, with the average household debt-service ratio (the percent of household disposable income spent to service debt payments) below pre-pandemic levels.

* Labor-market conditions remain healthy, even as some softening is expected ahead. Initial jobless claims have averaged roughly 221,000 thus far in 2025, well below the 30-year average of over 360,000. Nonfarm payrolls grew by a healthy 228,000 in March, well above consensus expectations for 130,000, while the unemployment rate rose modestly to 4.2%.

While recession risks have clearly risen, in our view an economic downturn is not a foregone conclusion. A strong starting point could provide support to the U.S. economy. Additionally, with monetary policy in restrictive territory, the Fed has ample room to cut rates if the economy shows meaningful signs of slowing.

-

The proposed tariffs could put upward pressure on inflation in the near term, as U.S. importers will

likely pass part of the cost from tariffs on to the consumer. During the 2018 – 2019 tariff announcements,

prices of goods rose modestly from low levels before subsiding shortly after. Based on the magnitude of

the tariffs announced last week, the impact on inflation will likely be more significant this time around.

However, there are potentially mitigating factors.

* Foreign manufacturers and U.S. importers or retailers could choose to absorb part of the cost instead of passing higher prices on to the consumer. However, for certain products where profit margins are slim, such as perishable food, any additional costs are more likely to be fully passed on to the consumer.

* U.S. importers may find substitutes for products when available, and over time supply chains may be altered or brought on-shore, although the latter will require investment and more time.

* A stronger U.S. dollar can make foreign goods cheaper in U.S. dollar terms and could partially offset the impact on prices. While this was the case during the targeted tariffs of 2018-2019, the U.S. dollar has weakened year-to-date despite the threat of tariffs.

Ultimately, we believe tariffs represent a one-time increase in prices as opposed to an ongoing source of inflation. The 10-year breakeven inflation rate, which is a market-based measure of expected inflation over the next 10 years, has fallen from 2.4% to below 2.2% since the end of March, near the low end of its three-year range. In our view, this signals that longer-term inflation expectations remain anchored and that downside risks to the economy likely outweigh the upside risks to inflation. This should give the Fed flexibility to lower rates if economic growth shows signs of slowing.

-

While the April 2 announcement provides some clarity into the U.S. administration's trade framework,

it remains uncertain as to how the impacted countries will respond. Some may take a similar approach

to China, retaliating with levies on U.S. exports, while others may seek negotiations to lower

tariff rates over time. We expect this process to play out in the weeks and months ahead, likely

keeping market volatility elevated in the near term.

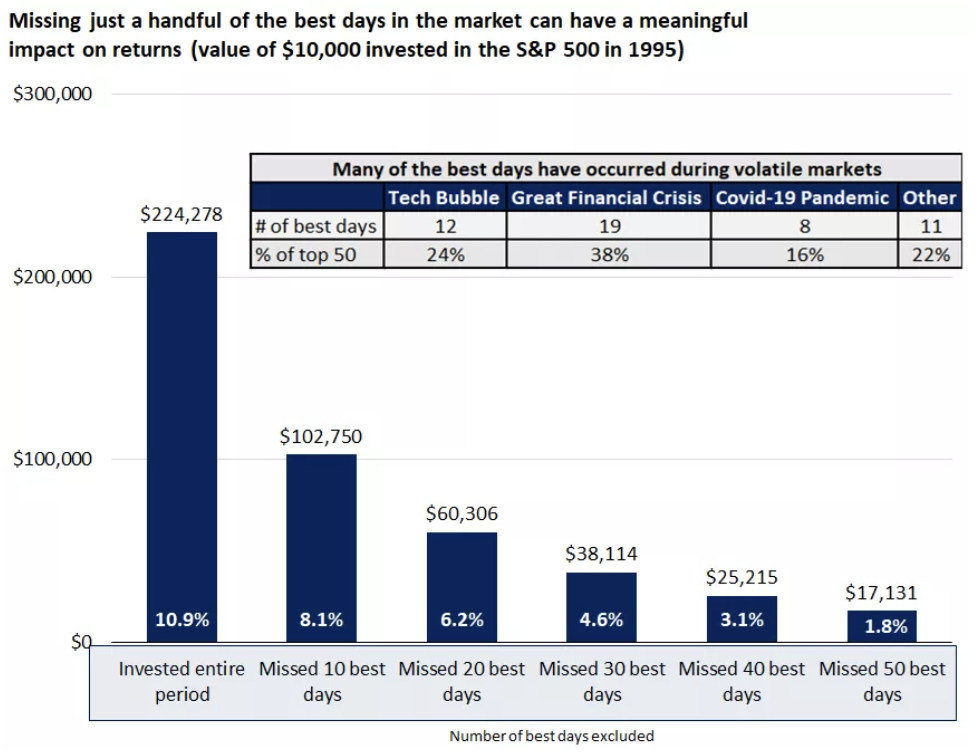

With uncertainty likely to remain in the coming weeks, we recommend investors resist the urge to make emotionally charged decisions, and instead stick with their long-term investment strategy. It's important to remember that on average, the S&P 500 experiences three to four pullbacks of 5% per calendar year and one pullback of 10% per year. Additionally, pullbacks of 15% occur on average once every two years, while pullbacks of 20% or more occur about once every three years.

Over the long run, we believe time in the market is a better investment strategy compared with timing the market. In fact, missing just a handful of the best days of the S&P 500 over the past 30 years would have led to meaningfully lower returns. What's more, many of the best days in the market have come during periods of market volatility, highlighting the importance of maintaining a long-term focus through turbulent markets.

-

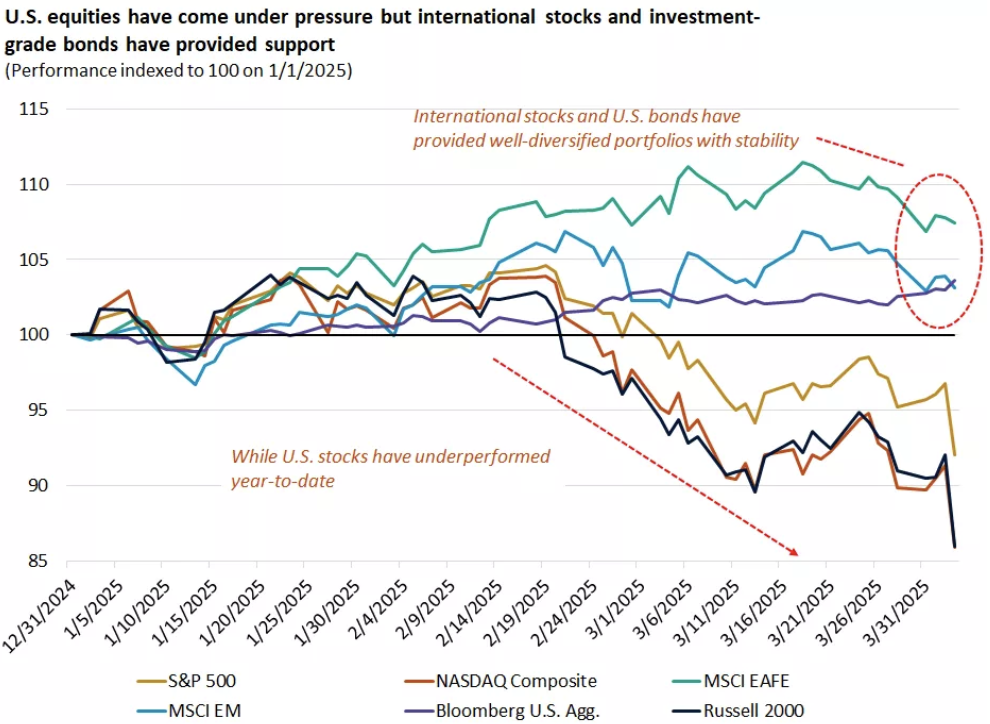

After two years that were dominated by outsized returns in U.S. large-cap stocks, diversification

has showed its merit in 2025. Despite volatility in U.S. equity markets, international stocks and

U.S. investment-grade bonds are positive year-to-date, helping offset the impact of U.S. stock

underperformance for investors with well-diversified portfolios. We believe diversification will

remain a key theme over the remainder of 2025. Incorporating allocations to a variety of different

asset classes can help smooth periods of volatility and help investors benefit from periods of

rotating leadership.

Within U.S. stocks, we recommend investors maintain balance between growth- and value-style investments. We believe opportunities are relatively attractive in the health care and financials sectors, which are two sectors potentially less exposed to tariffs. Additionally, we recommend investors maintain a strategic weight in U.S. investment-grade bonds, which have served as a safe-haven during market volatility.

While volatility is never comfortable, it is a normal part of investing. We believe investors are best served during this time by sticking with an investment strategy aligned to their financial goals as opposed to reacting to the short-term headlines.

-

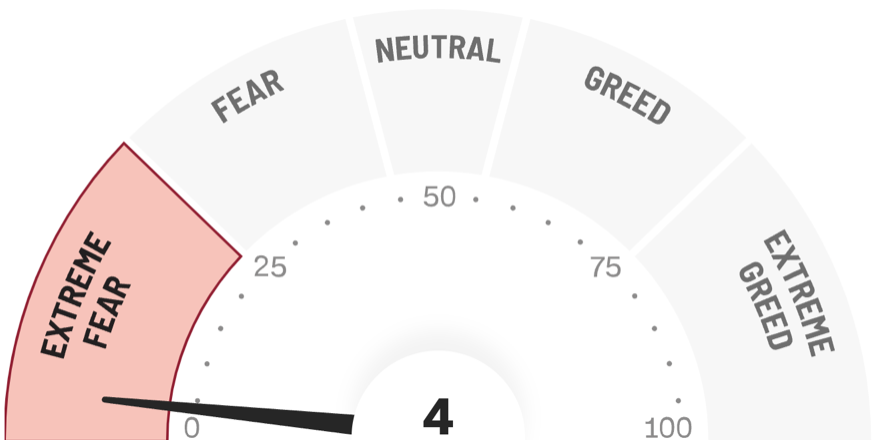

Final Words: Markets are down and fed is going to cut

interest rate, greed warranted. Buy VOO and VGT.

Below is CNN Greed vs Fear Index, pointing at 'Extreme Fear'.

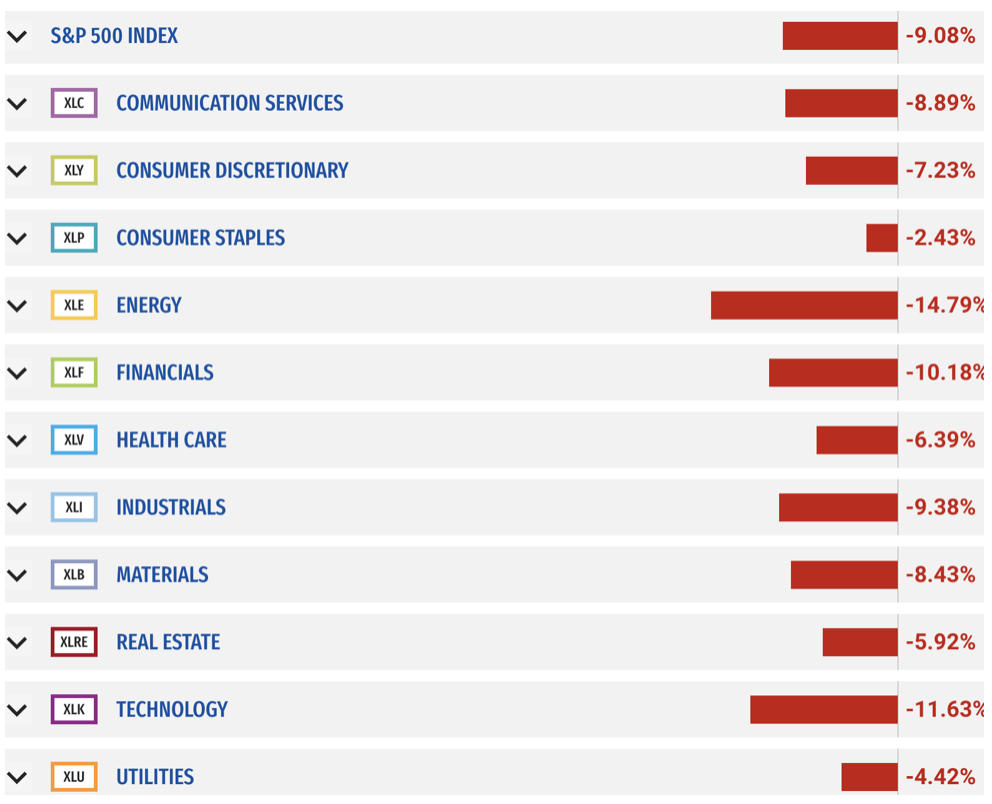

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

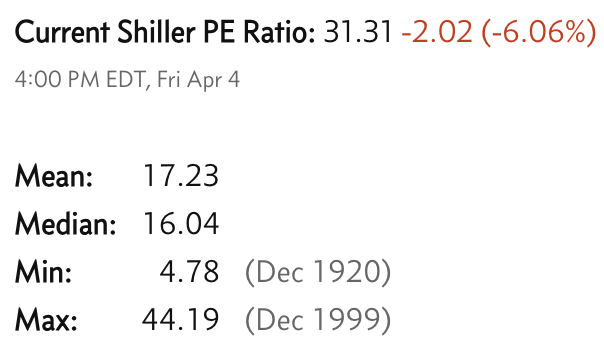

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.